Cyclemoneyco cash around is a digital financial tool designed to streamline peer-to-peer transactions. It enables users to send, receive, and manage funds through a mobile-first platform launched in 2021. Readers exploring cyclemoneyco cash around will also find context in Instagram Search Queries Optimization: Boost Visibility and Reach

Origins and Development of the Platform

The concept behind cyclemoneyco cash around emerged from a need to simplify informal money exchanges in urban communities. Founded by a team of fintech developers based in London, the service officially launched in March 2021 after two years of beta testing. com/cyclemoneyco-cash-around/” rel=”noopener noreferrer” target=”_blank”>CycleMoneyCo Cash Around: The Complete Guide to Flexible Cash Flow …

Early adopters included small vendors and freelance workers who relied on quick, low-fee transfers. The platform gained traction due to its minimal documentation requirements and compatibility with basic smartphones. Unlike traditional banking apps, it does not require a formal bank account to operate.

By mid-2022, the service had expanded to three additional European cities: Berlin, Lisbon, and Warsaw. Each location adapted the core model to comply with local financial regulations. This regional customization helped build trust among users and regulators alike.

How Cyclemoneyco Cash Around Functions

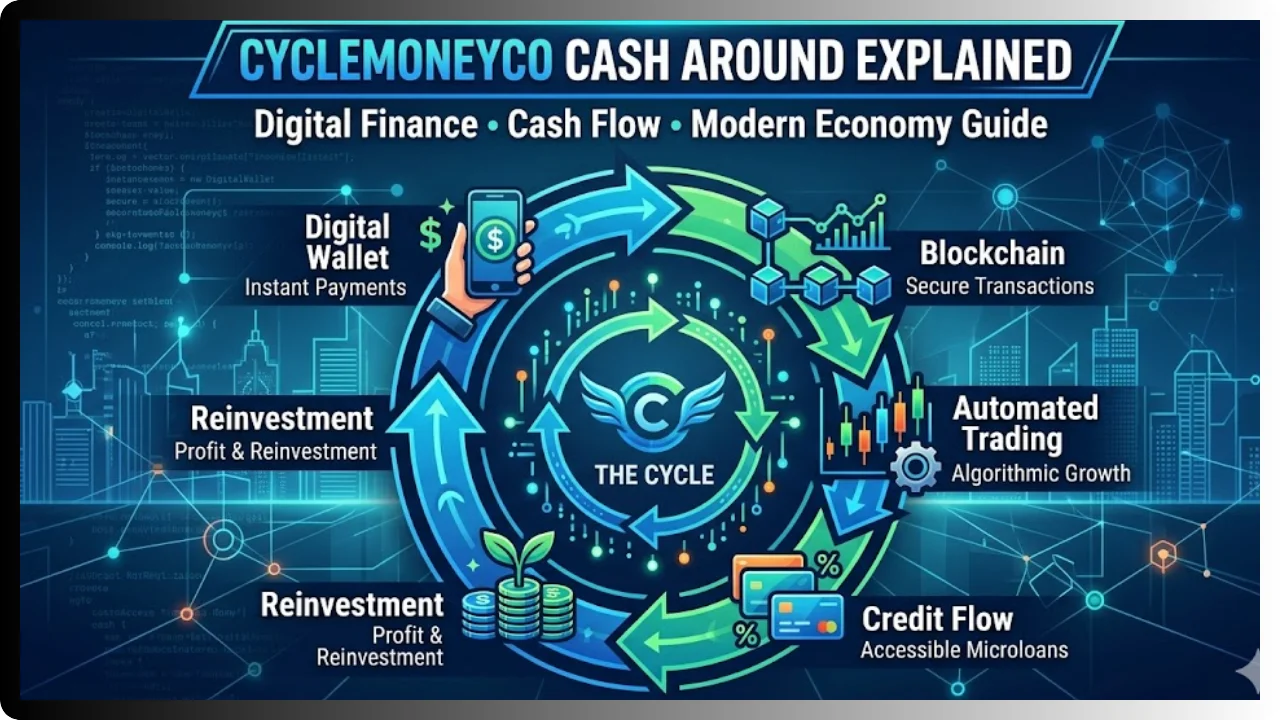

The interface allows instant transfers to other users by entering a recipient’s phone number or scanning a QR code.

Transactions are processed within seconds and incur a flat fee of €0.50 per transfer, regardless of amount. This pricing model appeals to users making frequent small payments, such as splitting bills or paying for services. The system uses end-to-end encryption to protect user data and transaction history.

One distinguishing feature is the “cash around” function, which lets users convert digital balances back into physical cash at designated pickup points. These locations include convenience stores, post offices, and mobile vans operating in underserved neighborhoods. This hybrid approach bridges digital and physical financial access.

What Is Confirmed and What Remains Unverified

The company has published quarterly transparency reports since its launch, detailing transaction volumes and user growth. Independent audits in 2022 and 2023 found no major security breaches or compliance violations.

However, the long-term sustainability of the flat-fee model remains uncertain. While the company claims operational costs are covered through partnerships and data analytics, it has not disclosed detailed financial statements. Some industry analysts question whether the current fee structure can support expansion without external funding.

Additionally, user privacy practices have drawn scrutiny. Although the platform states it does not sell personal data, its privacy policy allows for anonymized usage analytics to be shared with third-party advertisers. This has led to concerns among digital rights groups, though no formal complaints have been filed with regulatory bodies.

Why This Model Matters for Digital Inclusion

Cyclemoneyco cash around addresses a critical gap in financial accessibility. Millions of people remain unbanked or underbanked, particularly in urban areas with high migrant populations. Traditional banks often exclude these individuals due to documentation barriers or minimum balance requirements.

By offering a low-barrier entry point, the platform empowers users to participate in the digital economy. It supports everyday financial activities like paying rent, receiving remittances, or managing small business income. This inclusion can lead to greater economic resilience at the community level.

Looking ahead, the success of cyclemoneyco cash around may influence how regulators approach alternative financial services. If the model proves both secure and scalable, it could inspire similar initiatives in other regions. Policymakers are already monitoring its impact on financial literacy and digital adoption rates.

The platform’s emphasis on cash-in, cash-out flexibility also challenges the assumption that digital finance must eliminate physical money. Instead, it demonstrates that hybrid systems can meet diverse user needs. This balance may become increasingly important as digital payment adoption grows globally.

{kind=link}